The Transfer and Mortgaging of Immovable Property (Amending) (No. 2) Law introduces a crucial shift in the Cypriot legal framework governing foreclosures, specifically revising Article 44IA of the principal legislation. The Amendment of the Law has been published on 22.04.2026.

This specific amendment regulates the right of a mortgagee (e.g., a banking institution or a credit acquisition company) to purchase the mortgaged property themselves if it remains unsold within six months from the completion of the first auction.

The Legal Framework: Before and After the Amendment

-

The Previous Status Quo: Under the prior provisions of Article 44IA(2), if the mortgagee chose not to purchase the property themselves at its market value, they retained the right to proceed with subsequent sale efforts (either through follow-up auctions or direct sales) “without a reserve price”. From a legal perspective, this meant the property could potentially be liquidated at an excessively low price, leaving the debtor vulnerable to losing their asset without achieving any meaningful reduction or elimination of their remaining debt.

-

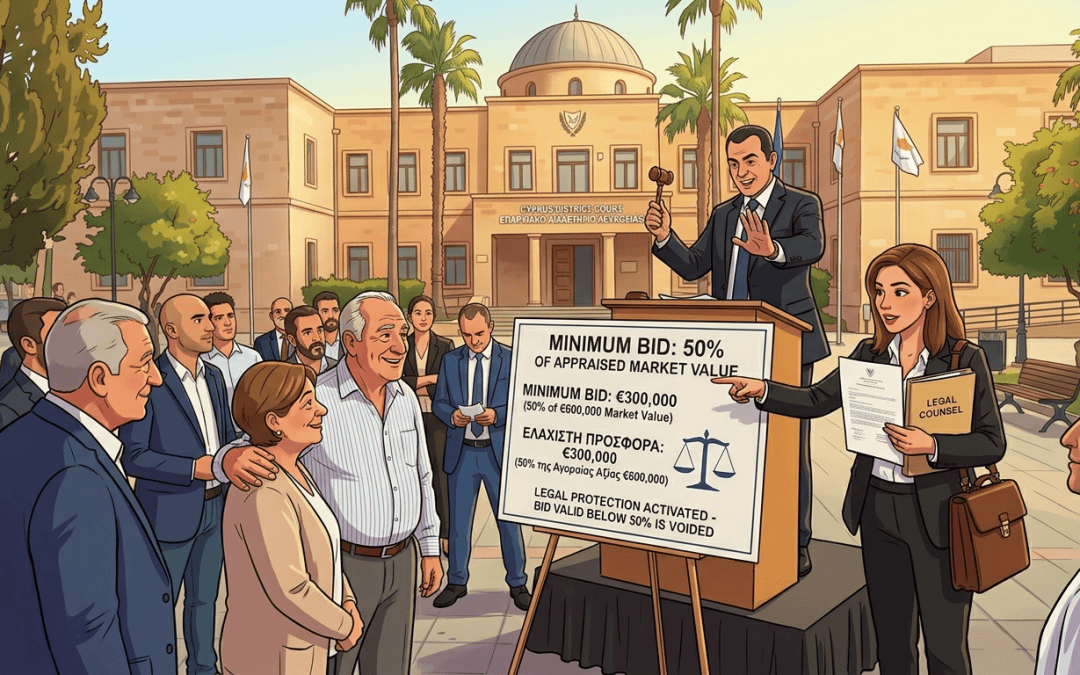

The New 2026 Regulation: The new amendment entirely deletes and replaces the phrase “without a reserve price”. It explicitly mandates that any subsequent attempts by the mortgagee to sell the property must be conducted “with a reserve price of not less than fifty percent (50%) of the market value of the mortgaged property.”

Legal and Economic Implications of the Amendment

The introduction of this 50% “floor” relative to the market value achieves three primary objectives:

- Protection of the Mortgagor (Debtor): It prevents the complete depreciation of the property’s value. Even if the asset fails to sell at the initial auction (where the reserve price is set at a minimum of 80%), the law now provides a safety net, ensuring that a citizen’s property cannot be liquidated for a nominal or “derisory” amount.

- Fair Debt Set-Off: Because the property cannot legally be sold below 50% of its current market value, the framework ensures that the ultimate amount credited against the borrower’s outstanding loan balance adheres to a fair, objective minimum standard.

- Equilibrium in the Foreclosure System: This amendment forces mortgagees to exercise greater diligence in their disposal procedures. By stripping creditors of the discretion to enforce unlimited price reductions, the law enhances transparency, equity, and balance within the Cypriot real estate market.

Summary: The amendment to Article 44IA represents a significant statutory intervention for the socio-legal protection of borrowers in Cyprus, putting a definitive end to foreclosures conducted without any reserve price.

For more information on this topic and assistance please contact its author, Mr. Andreas Parparinos at [email protected]